If you financed your solar system through a loan, there's a number in your contract that almost nobody told you about. It's called a dealer fee — and it may have added $5,000 to $15,000 to your loan balance before you signed a single page.

The CFPB has documented this practice across major solar lenders. It is not a fringe issue. It is standard operating procedure in the residential solar financing industry — and California homeowners are among the most affected.

How Dealer Fees Work

When you finance solar through a loan, the transaction works like this: the lender pays the installer directly for the system. But before that payment goes out, the lender adds a "dealer fee" — typically 10–30% of the system's cash price — to your loan balance.

The installer receives the cash price. You repay the cash price plus the dealer fee, plus interest on the entire inflated amount, over the life of the loan.

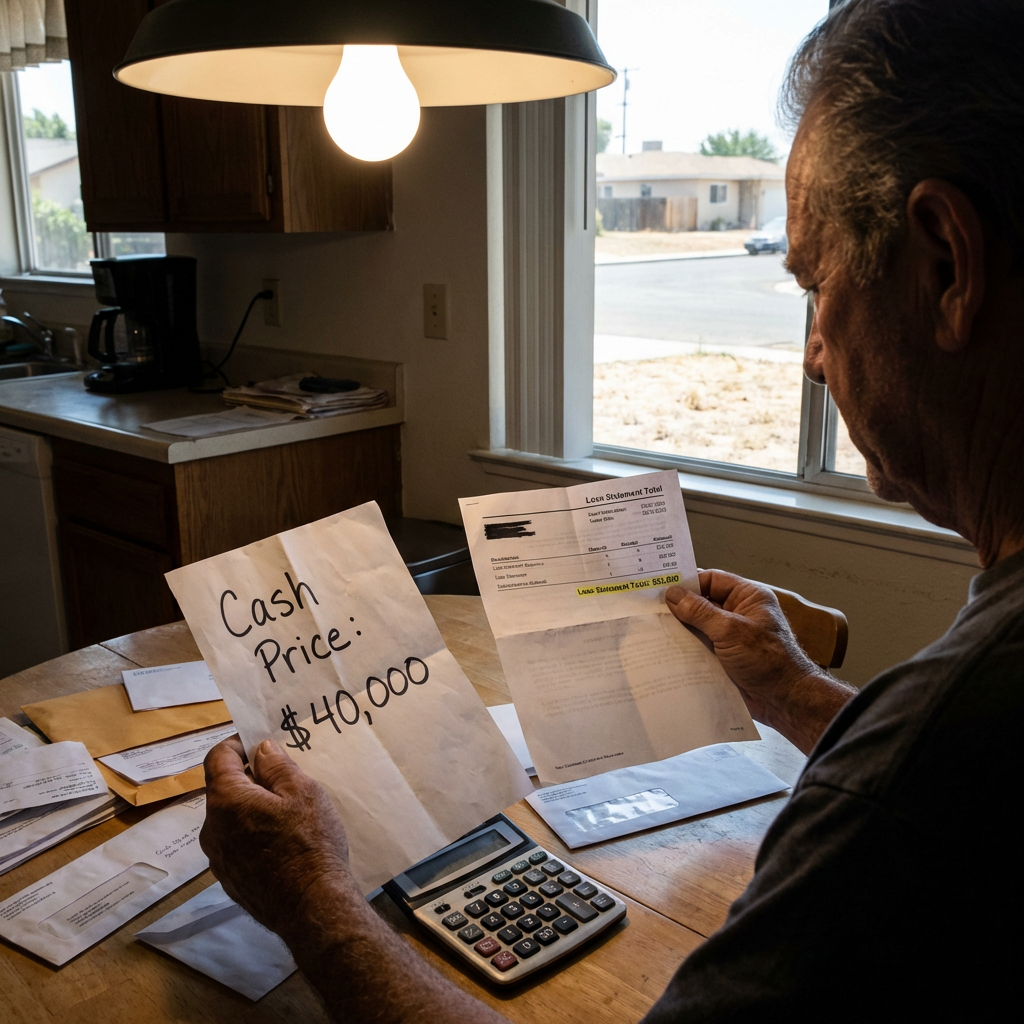

A system with a cash price of $40,000 becomes a $44,000–$52,000 loan. You pay interest on $52,000 — not $40,000. Over a 20–25 year loan at a typical solar APR, that difference compounds into tens of thousands of dollars in additional payments.

The dealer fee is rarely disclosed clearly. In many contracts it doesn't appear as a line item at all. The loan documents show a total financed amount — they don't show you that the cash price and the loan amount are two different numbers, or explain why.

Why This May Violate Federal Law

The Truth in Lending Act (TILA) and its implementing regulation, Regulation Z, require lenders to clearly disclose the true cost of credit — including APR, finance charges, total amount of payments, and the total financed amount broken down honestly.

A dealer fee that inflates the loan balance without clear disclosure may constitute an undisclosed finance charge under TILA. If the total amount financed in your loan documents doesn't accurately reflect the actual cost of the system plus properly disclosed fees, there is a potential TILA violation — one that can carry statutory damages, actual damages, and in some cases rescission of the loan entirely.

The CFPB, which oversees consumer financial products including solar loans, has published multiple reports specifically documenting hidden dealer fees and deceptive loan structures in solar financing. Their findings provide strong evidentiary support for consumer claims.

How to Find the Dealer Fee in Your Contract

Most homeowners don't know to look for this — which is exactly the problem. Here's how to check:

Step 1: Find the cash price of your system. This may appear in your original sales proposal, the installation agreement, or a separate purchase agreement. If the salesperson gave you a "cash price" vs. "financed price" comparison, the cash price is the baseline.

Step 2: Find the total loan amount in your financing documents. This is the amount you're actually borrowing — not the monthly payment, the total loan balance.

Step 3: Compare the two numbers. If the loan amount is more than 5–10% higher than the cash price, the difference is likely a dealer fee. A gap of 20–30% is a significant undisclosed markup.

Step 4: Check your APR. If your credit score would normally qualify you for a rate significantly lower than what's in your loan documents, the effective rate may be inflated by the dealer fee structure.

If you can't find a cash price anywhere in your documentation — that itself is a red flag. Some solar companies deliberately avoid putting the cash price in writing so the comparison can't be made.

The Lenders Most Associated With This Practice

The CFPB's reporting has specifically identified dealer fee practices across the major solar lending market, which in California has been dominated by lenders including Mosaic, GreenSky, Sunlight Financial, and EnerBank. This is not an accusation that every loan from these lenders is problematic — it's context for where to look if you're reviewing your own documents.

Frequently Asked Questions

Is a dealer fee illegal? Not inherently — fees paid to dealers exist in other lending contexts. What may be illegal is failing to disclose the fee clearly as required under TILA, or misrepresenting the total cost of the system during the sales process. The legality turns on disclosure, not existence.

Can I get my loan cancelled because of a hidden dealer fee? In some cases, yes. TILA violations can result in rescission — cancellation of the loan — particularly where the disclosure failures are material. This is fact-specific and depends on your loan documents, lender, and the severity of the undisclosed amounts.

What if I already paid off part of the loan? A TILA claim may still be available depending on when the violation is deemed to have occurred and your state's applicable limitations period. Document everything and get a professional review before assuming you're past the window.

My salesperson told me the dealer fee is just how solar financing works — is that true? It is how solar financing commonly works. That doesn't make it disclosed, legal, or something you simply have to accept. "Industry standard" is not a defense to a TILA violation or a consumer protection claim.

Think your loan balance is higher than the system was worth?

Book a free consultation or call

(213) 579-5156. We review solar loan documents across all of California — remote consultations available.