Latest insights

The Solar Tax Credit Lie: What California Homeowners Were Actually Promised

The Solar Tax Credit Lie: What California Homeowners Were Actually Promised

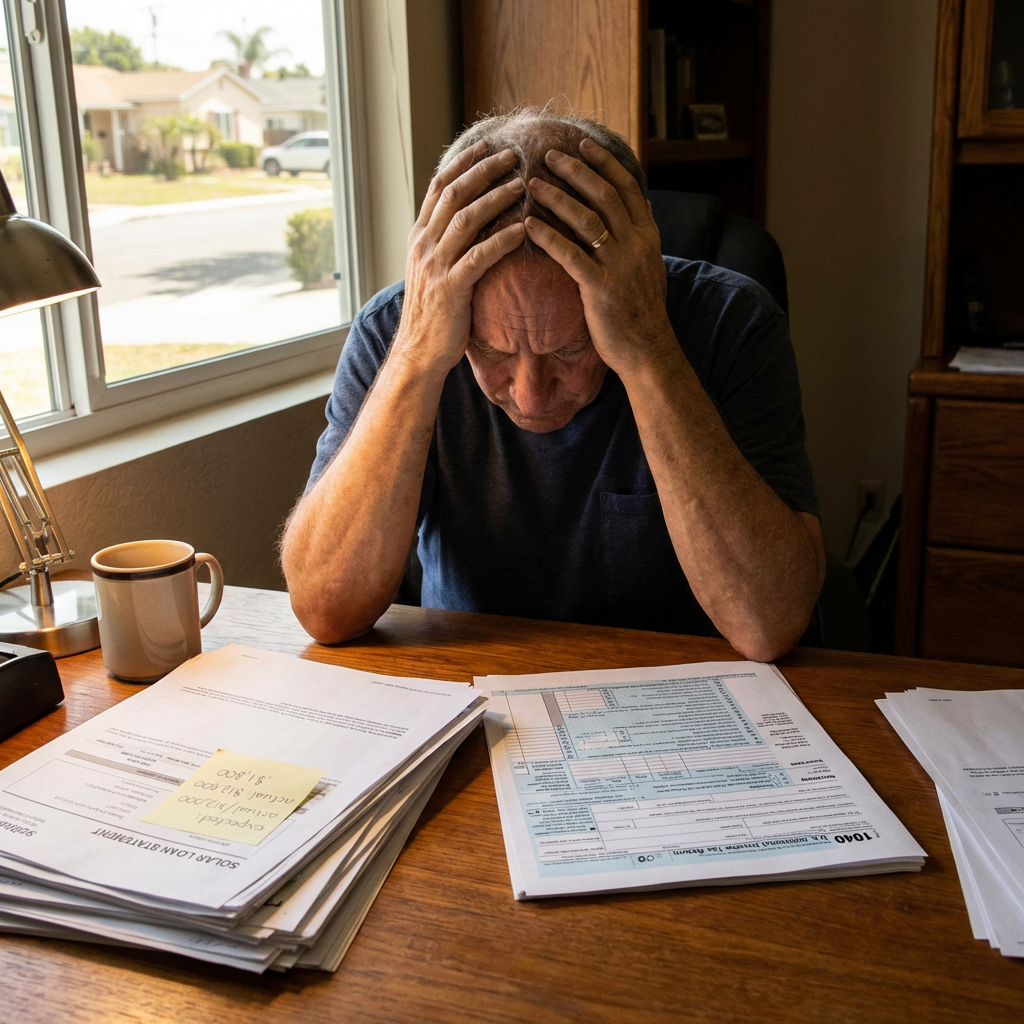

Of all the misrepresentations made during solar sales pitches, the federal tax credit claim may be the most damaging — because it sounds so specific and official that most homeowners never think to question it.

The pitch goes like this: "You'll receive a 30% federal tax credit that dramatically reduces your net cost. On a $40,000 system, that's $12,000 back." Sometimes it's framed as a check you'll receive. Sometimes it's built into a loan structure where you're expected to make a lump-sum payment in year one using the credit. Either way, millions of California homeowners signed contracts based on a version of the tax credit that doesn't work the way they were told.

What the Federal ITC Actually Is

The federal Investment Tax Credit (ITC) is a credit against taxes you owe — not a refund, not a check, not guaranteed money. This distinction is critical and is the source of enormous harm to homeowners who didn't understand the difference.

Here's how it actually works: if you purchase or finance a solar system, you may be eligible to claim 30% of the system cost as a credit on your federal income tax return. That credit reduces your tax liability dollar for dollar. If your total federal tax liability for the year is $8,000 and your credit is $12,000, you eliminate your tax bill entirely — but the remaining $4,000 doesn't come back to you as a refund. It carries forward to the following tax year.

If your tax liability is consistently low — as it is for retirees on fixed income, part-time workers, or anyone with significant deductions — you may never fully realize the credit you were promised. The credit doesn't expire, but it only offsets taxes you actually owe. If you never owe enough, you never get the full benefit.

Who Gets Hurt Most

The CFPB and consumer protection attorneys have identified a consistent pattern: solar companies disproportionately targeted seniors on fixed income and lower-income homeowners — precisely the populations least likely to have the tax liability needed to claim the full credit.

A retired couple receiving Social Security and a small pension may have a federal tax liability of $2,000–$4,000 per year. A salesperson who told them they'd receive a $12,000 tax benefit on a $40,000 system was either lying or dangerously uninformed. Either way, the homeowners made a financial decision based on money they were never going to see.

The Loan Structure That Makes It Worse

Many solar loans are specifically structured around the tax credit — and this is where the misrepresentation causes the most acute financial damage.

Here's how it works: the loan is written with artificially low initial payments for the first 12–18 months. The lender expects the borrower to apply their tax credit refund as a lump-sum principal reduction during that window. If they don't, the loan recasts — payments jump significantly, and the total interest owed increases dramatically.

Homeowners who were told they'd receive $12,000 from the IRS, applied it against the loan, and kept their payments low — only to discover their actual refund was $2,000 or zero — are now facing recasted loans with payments hundreds of dollars higher than they expected, on top of the tax credit they never received.

This is not a paperwork error. It is a foreseeable outcome of selling a tax-credit-dependent loan structure to someone who doesn't qualify for the full credit.

How to Check If This Happened to You

Look at your federal tax return for the year you installed solar. Find your total tax liability — not your refund, your liability. This is the number on line 24 of Form 1040 (or the equivalent for your filing year).

If your tax liability is less than 30% of your system's cash price, you didn't — and won't — receive the full credit in a single year. If the salesperson told you that you would, the projection was misrepresented.

Also check your loan documents. If your loan has a "required prepayment" or "expected federal tax credit payment" built into the structure — and you weren't clearly told that this payment was contingent on actually receiving the credit — that's a material disclosure failure.

What California Law Says

Misrepresenting how the federal ITC works — particularly telling a homeowner they'll receive a refund check when they won't — may constitute misrepresentation under California's Consumer Legal Remedies Act (CLRA) and Business and Professions Code Section 17200. These statutes don't require the company to have intended to deceive. A misleading statement that a reasonable person would rely on is sufficient.

For loan-structured misrepresentations involving the tax credit, TILA violations may also apply if the credit-dependent payment structure wasn't clearly disclosed as a condition of the loan terms.

Frequently Asked Questions

Can I still claim the ITC if I have a solar lease or PPA? No. If you don't own the system, you don't get the credit. The solar company that owns the equipment claims it. This is another common misrepresentation — homeowners in leases being told they'd receive a tax credit.

What if I was told the credit would come as a check from the IRS? That is factually incorrect. The ITC has never been a refundable credit — it cannot exceed your tax liability and does not generate a refund beyond that. If a salesperson told you otherwise, that is a misrepresentation regardless of whether they believed it themselves.

My loan recasted because I didn't make the lump-sum payment. What are my options? This is one of the most actionable situations California Solar Exit reviews. Depending on your loan documents and what you were told at signing, there may be grounds to challenge the loan structure itself. Document everything — your original sales materials, any written savings projections, and your loan agreement — before contacting anyone.

Is the 30% credit still available in 2026? Yes. The ITC is currently scheduled to remain at 30% through 2032 under the Inflation Reduction Act. Any salesperson who told you the credit was "expiring soon" to pressure a faster decision was misrepresenting the law.

Were you sold solar based on a tax credit you couldn't fully use? Book a free consultation or call (213) 579-5156. We review solar contracts and loan structures across all of California — remote consultations available.

Other insights

More from California Solar Exit